Introduction

With more than 60 amendments to the bill which was originally introduced, the Finance Bill 2023 has been passed by the Lok Sabha, on Friday, 23rd February 2023.

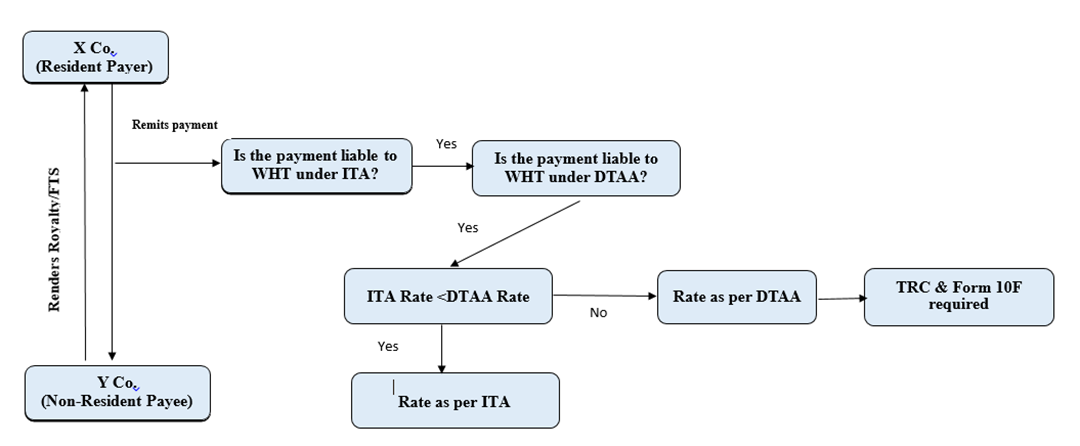

The increase in the withholding tax rate on royalties and fees for technical services from 10% to 20% (resulting in a maximum effective tax rate of 21.84% including surcharge and cess) took many firms off guard. To begin, refer to the graphical representation of a typical remittance transaction from Indian entities and let’s try to understand the terms mentioned therein:

1. Royalty

The Section 9 of the Income Tax Act defines Royalty as the transfer of any right or the granting of a license in respect of a patent, design, process, secret formula or similar property. It also takes in the imparting of any information concerning technical, industrial, commercial or scientific knowledge or skill and the use of patents, design, and so on.

2. Fee for Technical Services (FTS)

As per Section 9 of the Income Tax Act, “Fees for technical services” means any consideration (including any lump sum consideration) for the rendering of any managerial, technical or consultancy services (including the provision of services of technical or other personnel) but does not include consideration for any construction, assembly, mining or like project undertaken by the recipient or consideration which would be income of the recipient chargeable under the head “Salaries”.

The terms “managerial”, “technical” and “consultancy” have not been defined by the Act. However, by several decided case laws, we can derive a common element present in these services that enables us to classify under this specific category- which is “Human intervention”. Therefore, for a service to be categorized under FTS, there should be an element of human intervention.

3. Withholding tax (TDS)

Withholding Tax (WHT) or Tax deducted at Source (TDS), is an obligation on the tax-payers (either resident or non-resident) to withhold tax at the applicable tax rate when making payments of a specified nature, such as rent, commission, salary, professional services including royalty and fees for technical services, interest and so on.

4. Provisions related to WHT as per Income Tax Act, 1961 (ITA)

Section 195 of the Act addresses the provisions pertaining to withholding tax on payments made to non-residents. The withholding tax rate for royalty payments and FTS is provided in Part II of the First Schedule to relevant Finance Act. The Finance Bill 2023 – amendments to the Indian domestic tax law, includes an increase in the tax rate from 10% to 20% (plus surcharge and cess as applicable) on royalties and FTS for remittances from Indian entities.

5. Tax Treaty Benefits (DTAA)

According to section 90(2) of the Act, a taxpayer may opt to be governed by the Tax Treaty’s provisions if they are more advantageous than the Act’s provisions. These tax treaties are also referred as Double Tax Avoidance Agreements (DTAA).

Services provided by the non-residents are taxed in their home country (along with source country) as well, the Indian Government has entered into Double Taxation Avoidance Agreement (DTAA) with several countries. These DTAA shall contain the maximum rate of withholding tax at which certain services must be taxed.

6. Tax Residency Certificate (TRC)

For claiming this benefit, obtaining TRC (Tax Residency Certificate) is mandatory. A TRC is a certificate that is issued by the authorities of tax for the non-residents of that country declaring that the non-resident is a resident for that particular tax year for Double Taxation Avoidance Agreement (DTAA) applicability, and is eligible for tax benefits of the tax treaty.

7. Form 10F

Form 10F is Income tax form which is giving the benefit to non-resident tax payer to reduce the tax rate from higher rate to lower rate of TDS (tax deduction at source) in India. Form 10F is mandatorily filed by those NRI taxpayers who do not have the required details of the Tax Residency Certificate (mandated under the Double Taxation Avoidance Agreement). The documents required for Form 10F are as follows:

· Status (Individual, Company, Firm etc.)

· Permanent Account Number (PAN)

· Nationality (in case of an individual) or Country or specified territory of incorporation or registration (in the case of others);

· Tax Identification Number of the assessee, in the country of Residence or Unique Tax Identification Number;

· Period for which residential status is applicable;

· Address of the assessee in a country of residence.

· Digital signature certificate (DSC) is required to verify the Form 10F about the authentication of the information of the Form 10F.

Impact of change in WHT from 10% to 20% w.e.f 1st April 2023

1. Additional burden of filing income tax returns for the non-resident vendors

Under the erstwhile WHT rate of 10%, exemption from filing return of Income under Section 139(1) was available if the tax had been deducted at a rate NOT lower than that. However, if tax has been deducted at a rate lower than 10% by availing the beneficial provisions of DTAA, then, no exemption would be available from filing the return of income.

With the domestic tax rate being raised to 20%, foreign businesses are likely to rely on the lower rates specified in their respective tax treaties. This will necessitate more compliance on their part, such as acquiring a PAN, submitting income tax returns in India, receiving a TRC from their home country in order to claim tax treaty advantages, filing Form 10F and so on.

2. Increase in cost to the deductor if withholding tax is borne by him (i.e., grossing-up concept)

With the increased WHT rate, royalty charges and FTS would increase if the deductor is grossing up the withholding taxes, their expenses. According to Section 195A of the Act, if tax is to be borne by the payer, tax must be grossed up. For instance, if the invoice value is Rs.100, then the following table summarises the impact of the amendment:

| Particulars | Existing WHT | Effective from 1st April, 2023 |

| Invoiced value (INR) | 100 | 100 |

| Tax Rate* (Prescribed) | 10.40% | 20.80% |

| Tax Rate* (grossed up) | 11.61% | 26.26% |

| Effective cost (grossed-up) | 111.61 | 126.26 |

| Impact of grossing up | 11.61 | 26.26 |

| Increase in cost due to amendment | 14.65 |

*excluding the effect of surcharge and includes HEC @4%

3. WORST HIT! Payments to non-residents of countries which has no tax treaty with India

According to tax experts, the unexpected move to double the withholding tax rate will force companies to take advantage of tax treaty benefits, which have a high compliance burden and were previously underutilised because domestic rates were mostly equal to or higher than the respective treaty rates. The greatest impact will be felt in circumstances where payments are made to companies in countries with which India does not have a tax treaty.

4. Not enough time to digest and implement the move

Tax treaty benefits will become even more important today in order to obtain a lower withholding tax rate. To be eligible for such treaty benefits, foreign businesses must assess their commercial substance. This may also raise the cost of technology imports in circumstances where Indian enterprises are subject to withholding taxes and treaty benefits are not available

The amendment would be effective from 1st April 2023, giving less time to the Indian entity and its foreign affiliates or non-affiliate foreign parties to restructure their contractual terms.

Analysis of Tax treaties vis-à-vis Income Tax Act w.e.f 1st April 2023

A. Royalties

| Country | Article No. | WHT per Tax Treaty | WHT per IT Act 1961 *1 | Beneficial WHT Rate |

| Australia | 12 | 10|15 % *2 | 20% | Tax Treaty – 10|15% |

| Brazil | 12 | 25% – Trademarks15% – Others | 20% | Income Tax Law – 20% for use of TrademarksFor others Tax Treaty – 15% |

| Canada | 12 | 10|15 % *2 | 20% | Tax Treaty – 10|15% |

| China | 12 | 10% | 20% | Tax Treaty – 10% |

| France | 13 | 10% | 20% | Tax Treaty – 10% |

| Germany | 12 | 10% | 20% | Tax Treaty – 10% |

| Italy *3 | 13 | 20% | 20% | Tax Treaty – 20% |

| Korea | 12 | 10% | 20% | Tax Treaty – 10% |

| Malaysia | 12 | 10% | 20% | Tax Treaty – 10% |

| Netherlands | 12 | 10% | 20% | Tax Treaty – 10% |

| Singapore | 12 | 10% | 20% | Tax Treaty – 10% |

| South Africa | 12 | 10% | 20% | Tax Treaty – 10% |

| Switzerland | 12 | 10% | 20% | Tax Treaty – 10% |

| UK | 13 | 10|15 % *2 | 20% | Tax Treaty – 10|15% |

| USA | 12 | 10|15 % *2 | 20% | Tax Treaty – 10|15% |

B. Fees for Technical Services

| Country | Article No. | WHT per Tax Treaty | WHT per IT Act 1961 *1 | Beneficial WHT Rate |

| Australia | 12 | 10|15 % *2 | 20% | Tax Treaty – 10|15% |

| Brazil | 12 | 25% – Trademarks15% – Others | 20% | Income Tax Law – 20% for use of Trademarks For others Tax Treaty – 15% |

| Canada | 12 | 10|15 % (Note 2) | 20% | Tax Treaty – 10|15% |

| China | 12 | 10% | 20% | Tax Treaty – 10% |

| France | 13 | 10% | 20% | Tax Treaty – 10% |

| Germany | 12 | 10% | 20% | Tax Treaty – 10% |

| Italy *3 | 13 | 20% | 20% | Tax Treaty – 20% |

| Korea | 12 | 10% | 20% | Tax Treaty – 10% |

| Malaysia | 12 | 10% | 20% | Tax Treaty – 10% |

| Netherlands | 12 | 10% | 20% | Tax Treaty – 10% |

| Singapore | 12 | 10% | 20% | Tax Treaty – 10% |

| South Africa | 12 | 10% | 20% | Tax Treaty – 10% |

| Switzerland | 12 | 10% | 20% | Tax Treaty – 10% |

| UK | 13 | 10|15 % *2 | 20% | Tax Treaty – 10|15% |

| USA | 12 | 10|15 % *2 | 20% | Tax Treaty – 10|15% |

Notes to analysis of tax treaties vis-à-vis Income Tax Act w.e.f 1st April 2023:

1. Taxable Rate as per Income Tax law would be further increased by applicable Surcharge and Cess, Maximum effective tax rate would be 21.84%.

2. Multiple Withholding Tax rates per Tax Treaty:

a. Australia

The 10% rate applies to royalties paid (i) for the use of, or the right to use, industrial, commercial, or scientific equipment and (ii) in consideration for the total or partial forbearance in respect of the use or supply of such equipment; otherwise, the rate is 15%.

b. Canada

The 10% rate applies to payments for the use of, or the right to use, industrial, commercial, or scientific equipment; otherwise, the rate is 15%.

c. United Kingdom

The 10% rate applies to royalties paid for the use of, or the right to use, industrial, commercial, or scientific equipment other than income derived by an enterprise from the operation of ships or aircraft in international traffic; the 15% rate applies to royalties paid for the use of, or the right to use, a copyright of literary, artistic, or scientific work, including cinematographic films or work on films, tape, or other means of reproduction for use in connection with radio or television broadcasting, a patent, trademark, design or model, plan, secret formula or process, or for information concerning industrial, commercial, or scientific experience.

d. USA

The 10% rate applies to royalties paid for the use of, or the right to use, industrial, commercial, or scientific equipment other than income derived by an enterprise from the operation of ships or aircraft in international traffic; the 15% rate applies to royalties paid for the use of, or the right to use, a copyright of literary, artistic, or scientific work, including cinematographic films or work on films, tape, or other means of reproduction for use in connection with radio or television broadcasting, a patent, trademark, design or model, plan, secret formula or process, or for information concerning industrial, commercial, or scientific experience, including gains derived from the alienation of any such right or property that are contingent on their productivity, use, or disposition.

3. Tax treaty rate for Italy is 20% whereas effective tax rate as per Income Tax law is 20% plus applicable surcharge and cess, thus WHT as per Tax treaty is beneficial.

In case you need any help please drop an email to nikhil@bclindia.in or rakesh@bclindia.in